Hubbard Radio Washington DC, LLC. All rights reserved. This website is not intended for users located within the European Economic Area.

Financial planner Arthur Stein has many clients who are TSP investors, even several TSP millionaires. He offered advice in today's guest column.

Many Thrift Savings Plan investors consider the treasury securities G fund the safest investment option they have. During the Great Recession, tens of thousands moved from the stock indexed C, S and I funds into the safety of the G fund. Many never returned even though the market bounced back big time.

Financial planner Arthur Stein has many clients who are TSP investors, even several TSP millionaires. He offered advice in today’s guest column:

The G fund is often described as the safest of the TSP investment funds. Sometimes it is called the “super safe” G fund that “never has a bad day.” It invests in short-term, non-marketable U.S. Treasury securities guaranteed by the federal government.

As a result, TSP participants keep a higher portion of their TSP balances in the G fund than any other fund.

|

||||||||||||||||||||||||||||

However, there are many types of investment risk. The only guarantees provided by the G fund are the lack of volatility — fluctuations in value — and the guarantee against loss of principal provided by the government. None of the other TSP funds offer those guarantees. More information on volatility and TSP Fund returns can be found on my website.

Historically, using the G fund as a long-term investment exposed investors to a higher risk of losing purchasing power. The rate of return for the G and F funds was not sufficient to increase purchasing power after subtracting out the negative effects of inflation and taxes on withdrawals.

The loss of purchasing power may not be noticed until withdrawals are needed to supplement the federal annuity and Social Security.

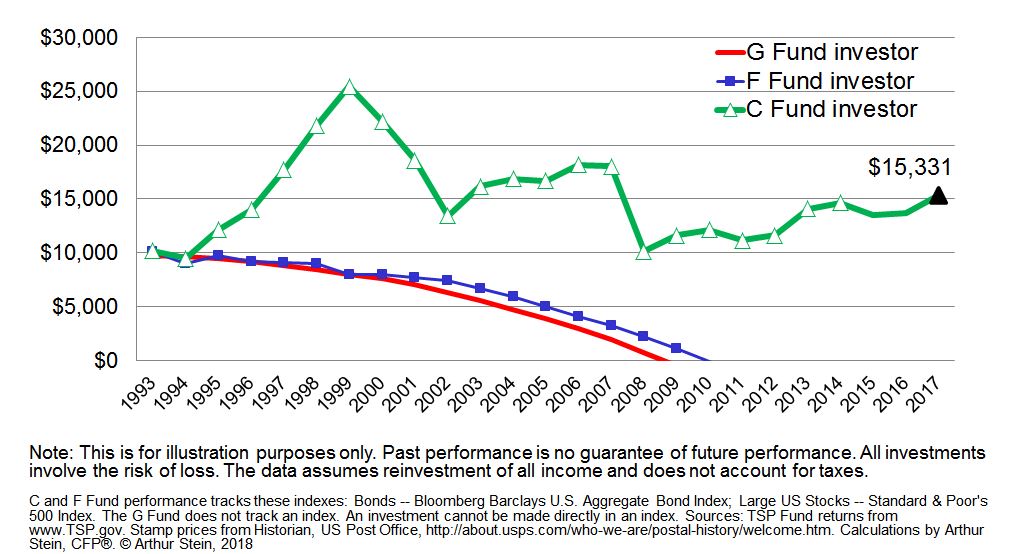

For example, at the beginning of 1993, retirees Bill, Jack and Mary each had $10,000 in the TSP. Each invested their $10,000 in one fund:

• Bill in G (short-term US Treasury securities),

• Jack in F (government and corporate bonds) and

• Mary in C (stocks of large US companies).

Each year they annually withdrew the same dollar amount, enough to buy 2,000 first class stamps, after paying taxes of 30 percent on the withdrawals.

Why First Class stamps? They are are unique in that the value (service provided) is the same year after year. Thirty years ago, one First Class stamp was sufficient to mail a letter anywhere in the U.S. and the same is true today. That makes First Class stamps a good proxy for inflation.

The graph below shows what happens to the TSP balances of Bill, Jack and Mary as a result of the annual withdrawals.

Stein will be the guest today on our Your Turn radio show, which airs 10 a.m. on www.federalnewsradio.com or on 1500 AM in the metro Washington area. If you have questions for them send them to me before showtime at mcausey@federalnewsradio.com

By Amelia Brust

Maine has a unique natural phenomenon for New England: a 40-acre desert outside the town of Freeport. When the Tuttle family began farming on the then-300-acre property in 1797, they neglected to rotate crops, conducted a massive clearing and allowed for overgrazing of livestock. The effects were severe soil erosion which exposed a hidden desert. The site is now a tourist attraction.

Source: Desert of Maine

Copyright © 2024 Federal News Network. All rights reserved. This website is not intended for users located within the European Economic Area.

Mike Causey is senior correspondent for Federal News Network and writes his daily Federal Report column on federal employees’ pay, benefits and retirement.

Follow @mcauseyWFED